The recent escalation of the U.S. trade disputes with China and Mexico is putting Federal Reserve policymakers in a bind. This comes at a time when global economic growth is losing its momentum, and the effects of President Trump’s tax cuts are wearing off. The International Monetary Fund projected that the current and threatened U.S.-China tariffs could slash global GDP by 0.5% in 2020. This slow-down is most noticeable in the Eurozone and Japan. As for the Chinese economy, the outlook for growth is becoming less certain.

The Fed has held its benchmark rate steady so far this year in a range between 2.25% and 2.50%. However, with risks to the multi-year U.S. expansion rising, Fed officials recently started debating whether and when to cut the rates. They already expect the economy to slow down by 1% to around 2% growth from last year to this year. Any forecast of a sharper-than-expected decline would fuel concerns of recession.

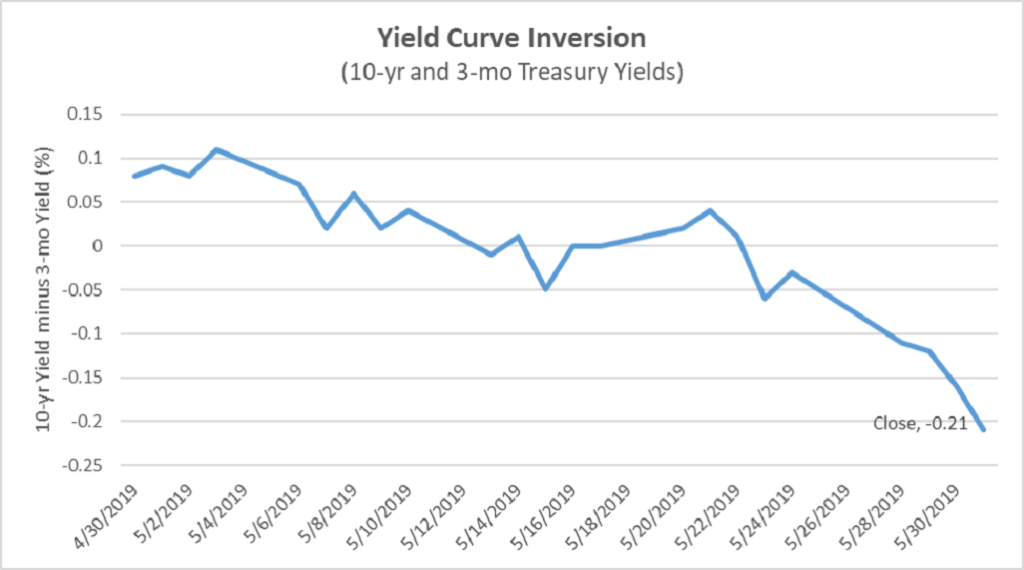

The change in sentiment has already convinced bond investors that a rate cut is likely as bond yields have pushed lower in recent weeks. The 10-year Treasury yield was down to 2.142% at the end of May, and it currently sits well below yields on three-month Treasuries. This represents a so-called yield-curve inversion (Exhibit I) which often precedes rate cuts and recessions as investors prefer to lock in higher rates.

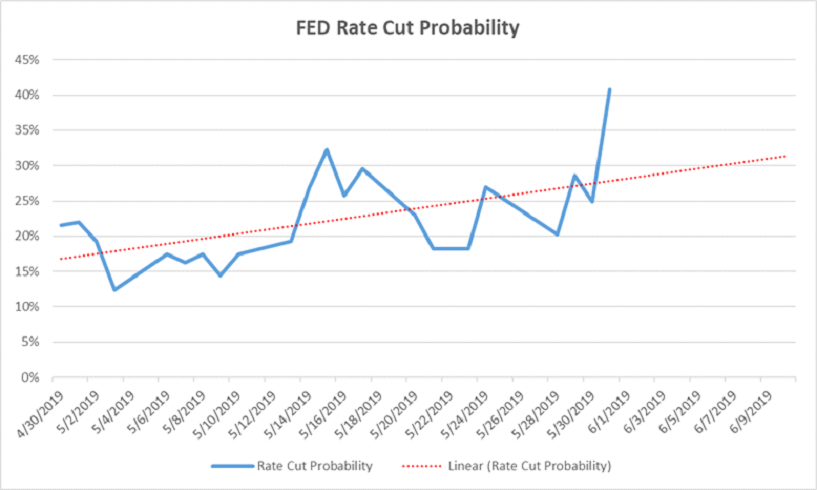

Futures markets provide further evidence that a rate decline is expected. As of the time of this writing, the CME FedWatch tool places about a 25% chance of a 25-basis point rate cut at the Fed’s June meeting and an 80% chance of at least a 25-basis point decline from current levels at their July meeting. The CME FedWatch tool computes probabilities for future interest rate levels based on Fed Funds Futures prices. Market expectations are factored into these prices. As can be seen from Exhibit II, the probabilities of a rate decline have been trending upwards since the start of May with expectations spiking at the end of the month.

Fed policymakers have always had a challenging task. Congress maintains three key objectives for the Federal Reserve: to maximize employment, stabilize prices, and moderate long-term interest rates. For example, the Fed must encourage low unemployment while also monitoring nominal wage increases to make sure that inflation does not grow out of control. They must also ensure that in the long run, interest rates are not too low or too high. And now, the United States is only recently coming out of a period of unprecedented quantitative easing, complicating matters further for current policymakers. The bottom line is this: Fed officials must balance the risks of easing too soon with the costs of waiting too long; and a wrong decision may have far reaching consequences.

The views expressed represent the opinion of Passage Global Capital Management, LLC. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute as investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Passage Global Capital Management, LLC believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Passage Global Capital Management, LLC’s views as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumption that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements.